Documentação Geral

Parametrização Fiscal – Passo D0049-3 – IPI – Alteração retorno de crédito na aquisição por equiparado de bebidas, perfumaria e cosméticos

Parametrização Fiscal – Passo D0049-3 – IPI - alteração retorno de crédito na aquisição por equiparado de bebidas, perfumaria e cosméticos

Por Fernanda Penhorate

Através de uma solicitação da P&G, fizemos uma melhoria no retorno de crédito de IPI que funciona da seguinte forma:

No cenário de entrada cujo remetente contém perfil 1 ou 24 e o destinatário é o 138 (no destino fechamos que tem que ser exatamente o 138), como regra geral o atacadista (138) que está adquirindo não tem direito ao crédito de IPI, pois sua saída posterior não é tributada pelo IPI.

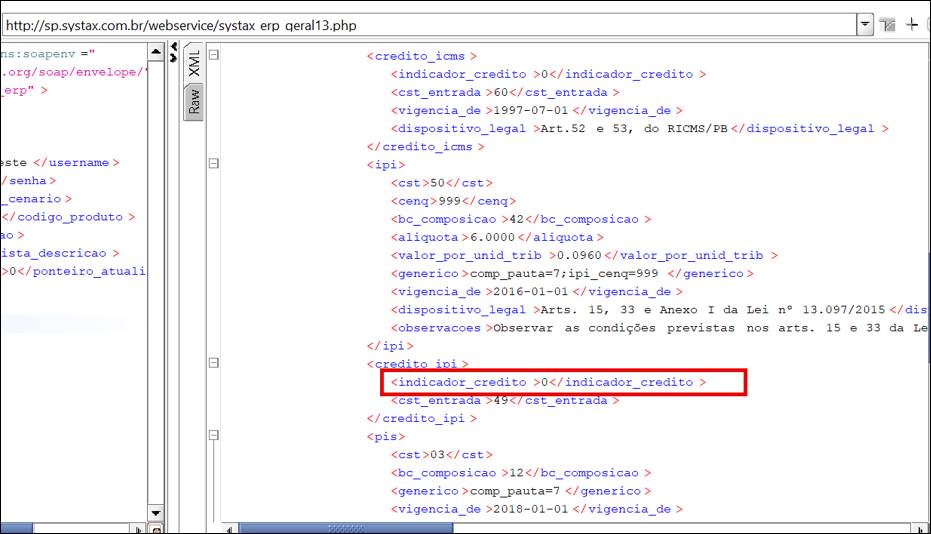

Então nessa operação entregamos o indicador de 0, pois é a regra aplicável.

Ocorre que existe a hipótese desse atacadista ser equipado a industrial, e nesse caso em questão estamos falando somente do equiparado de produtos de perfumaria, cosméticos e bebidas.

Logo, sua saída subsequente é tributada pelo IPI, o que na ocasião da compra da indústria ou do importador lhe dá direito a crédito, algo que até hoje não estávamos entregando.

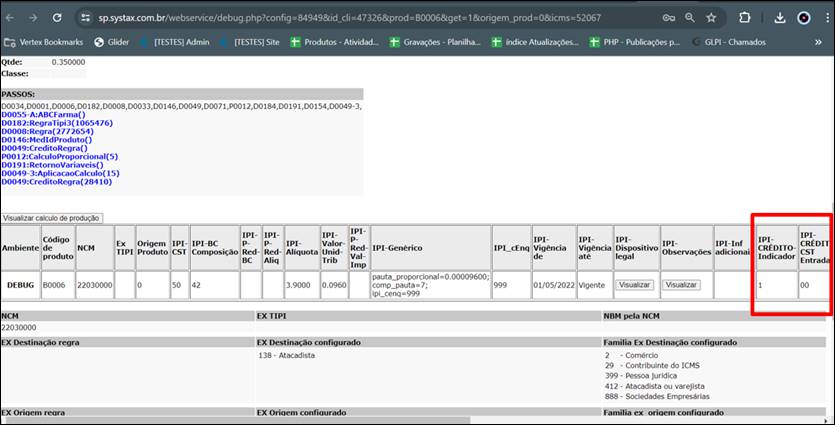

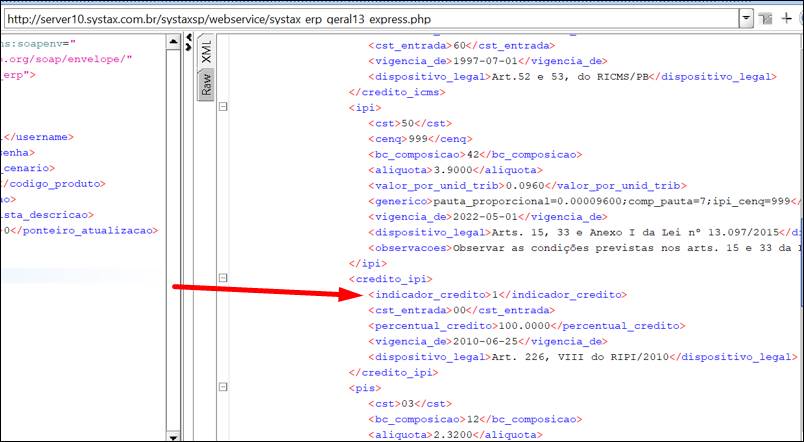

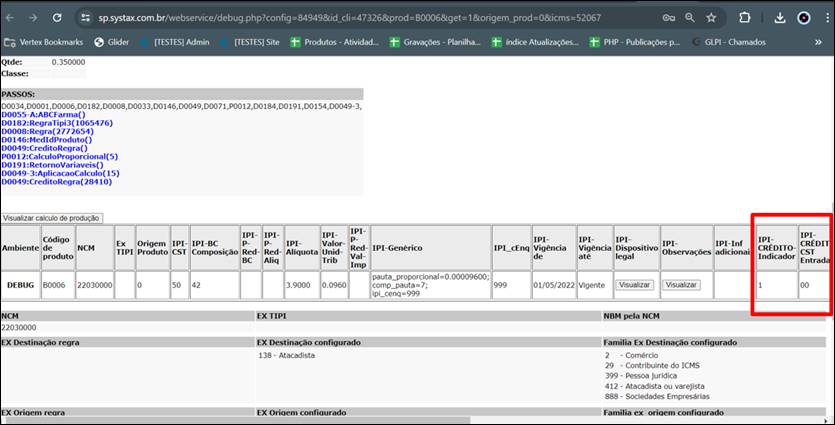

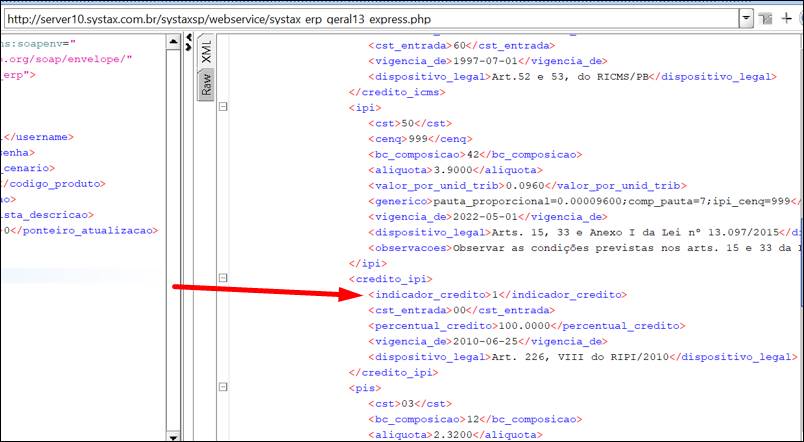

Para entregarmos esse crédito por ocasião da entrada, foi preciso fazer uma implementação na parametrização fiscal, assim sempre que o cenário houver perfil origem contém o 1 ou 24 e destinação o 138, o cálculo incluíra o perfil destino, ex_destinação 2972, por meio do passo D0049-3, para busca de regra de crédito, e com isso encontrará uma regra de crédito com indicador 1 para os produtos que for equiparado.

O ex_destinação 2972 foi criado para essa manobra da busca de regra de crédito, não é necessário incluir no cenário, mas caso seja incluído, sempre buscará a regra de crédito citada.

Como o cálculo da regra na parametrização fiscal é feito no cenário e produto da base centralizada, todos os retornos de IPI consultados no debug terá esse retorno. O mesmo ocorrerá com que é demais projetos.

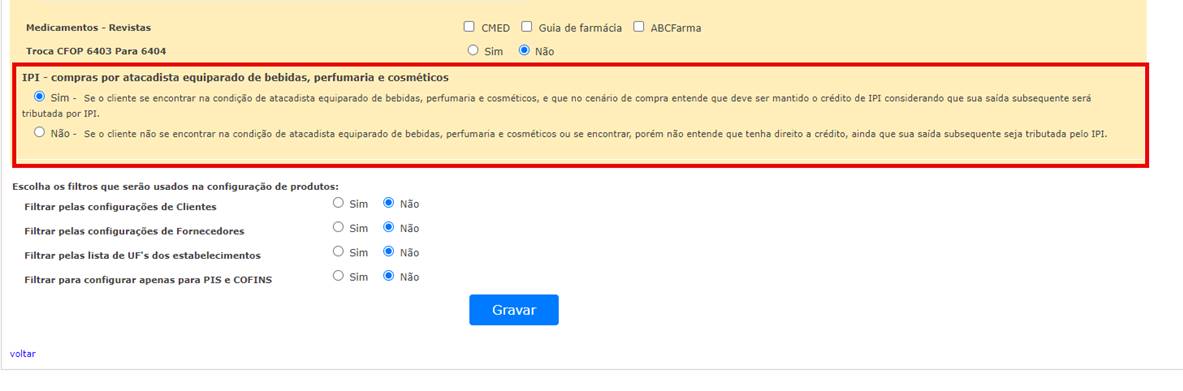

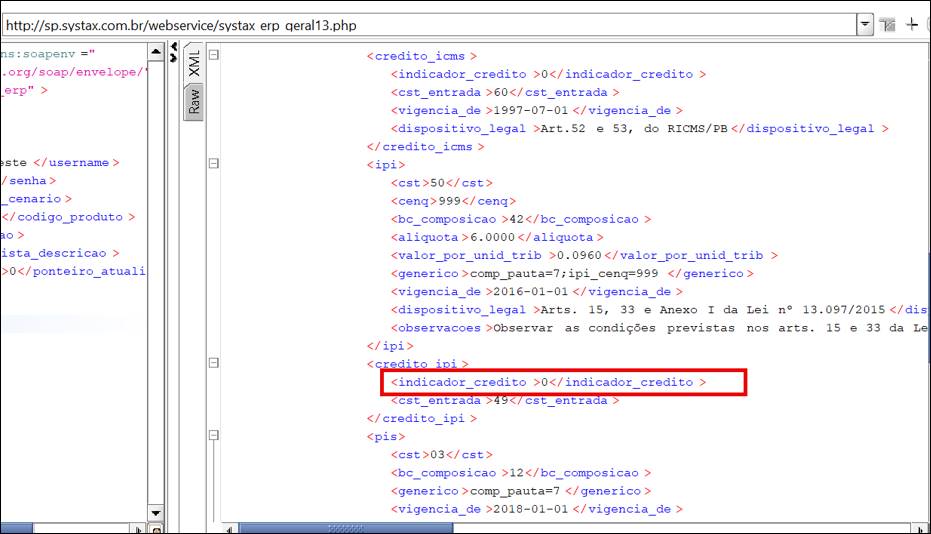

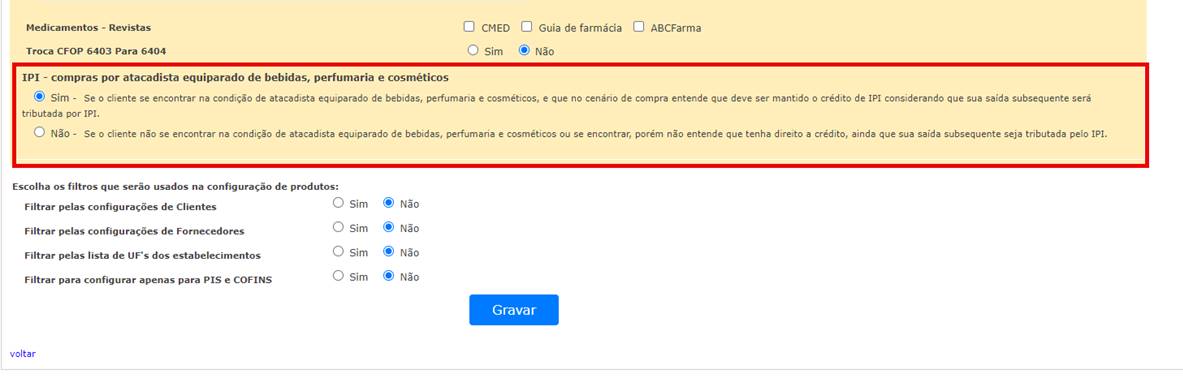

Como esse não é o entendimento de todos os clientes, não podemos entregar isso para todos, por isso criamos uma flag no cadastro das empresas, onde esse retorno pode ser alterado, de forma que trocamos o retorno para indicador de crédito=0 (como já é hoje).

Flag no cadastro:

Retorno:

Resumindo:

Todo cenário de entrada com perfil origem contém 1 ou 24 e perfil destino igual 138, troca o retorno de crédito de 0 para 1, se encontrar a regra com perfil destino 2972.

Se a Flag “IPI – compras por atacadista equiparado de bebidas, perfumaria e cosméticos” estiver ativa = mantem a entrega da regra de crédito de IPI com indicador 1.

Se a Flag “IPI – compras por atacadista equiparado de bebidas, perfumaria e cosméticos” NÃO estiver ativa = troca a entrega da regra de crédito de IPI com indicador 0 (troca no webservice, cálculo online (on demand, carga expressa, csv Vertex e csv Carrefour).

Assim, garante o retorno adequado para a empresa que deseja a troca, e mantém o retorno atual para os clientes que não devem ser submetidos a ela.

D0049-3 Step – IPI – Change in return of credit on acquisition of beverages, perfumery, and cosmetics by the equivalent of an industrial facility

By Fernanda Penhorate

Through a request from P&G, we made an improvement in the return of IPI credit that works as follows:

In the input scenario where the sender has profile 1 or 24 and the recipient is 138 (at the destination, we closed that it must be exactly 138), as a general rule, the wholesaler (138) who is acquiring does not have the right to IPI credit, as their subsequent exit is not taxed by IPI.

So, in this operation, we deliver indicator 0, as it is the applicable rule.

It so happens that there is a hypothesis that this wholesaler is equivalent to an industrial facility, and in this case, we are talking only about the equivalent of perfumery, cosmetics, and beverage products.

Therefore, their subsequent exit is taxed by IPI, which at the time of purchase from the industry or importer gives them the right to credit, something that until today we were not delivering.

To deliver this credit on entry, it was necessary to implement a change on fiscal parameterization, so whenever the scenario has an origin profile containing 1 or 24 and destination 138, the calculation will include the destination profile, ex_destination 2972, through step D0049-3, to search for a credit rule, and with that, it will find a credit rule with indicator 1 for the products that are equivalent.

The ex_destination 2972 was created for this maneuver of searching for a credit rule, it is not necessary to include it in the scenario, but if it is included, it will always search for the mentioned credit rule.

As the rule calculation in fiscal parameterization is done using the scenario and product of the centralized base, all IPI returns consulted in debug will have this return. The same will happen with other projects.

As this is not the understanding of all clients, we cannot deliver this to everyone, so we created a flag in the company profile, which if active will keep the return with credit indicator 1, but if turned off will change the return to credit indicator 0 (as it is today).

Flag in the profile:

Return:

In summary, every input scenario with origin profile containing 1 or 24 and destination profile equal to 138, changes the credit return from 0 to 1, if it finds the rule with destination profile 2972.

If the flag "IPI - purchases by equivalent wholesaler of beverages, perfumery, and cosmetics" is active = keeps the delivery of the IPI credit rule with indicator 1.

If the flag "IPI - purchases by equivalent wholesaler of beverages, perfumery, and cosmetics" is not active = changes the delivery of the IPI credit rule with indicator 0 (exchange in the webservice, online calculation, on-demand, express load, CSV vertex, and CSV Carrefour).

Thus, it guarantees the appropriate return for the company that wants the exchange and maintains the current return for clients who should not be submitted to it.

| Versão do documento: 66 | Publicação: 6/28/2024 |