Documentação Geral

Parametrização Fiscal – Retorno do cBenefRBC

Retorno do cBenefRBC

Por Carlos Dupim Jr.

Para um produto e cenário existe a possibilidade de aplicação de regra com CST 51 e CST 20, o sistema pelo critério de desempate por regra mais benéfica aplica a regra do CST 51.

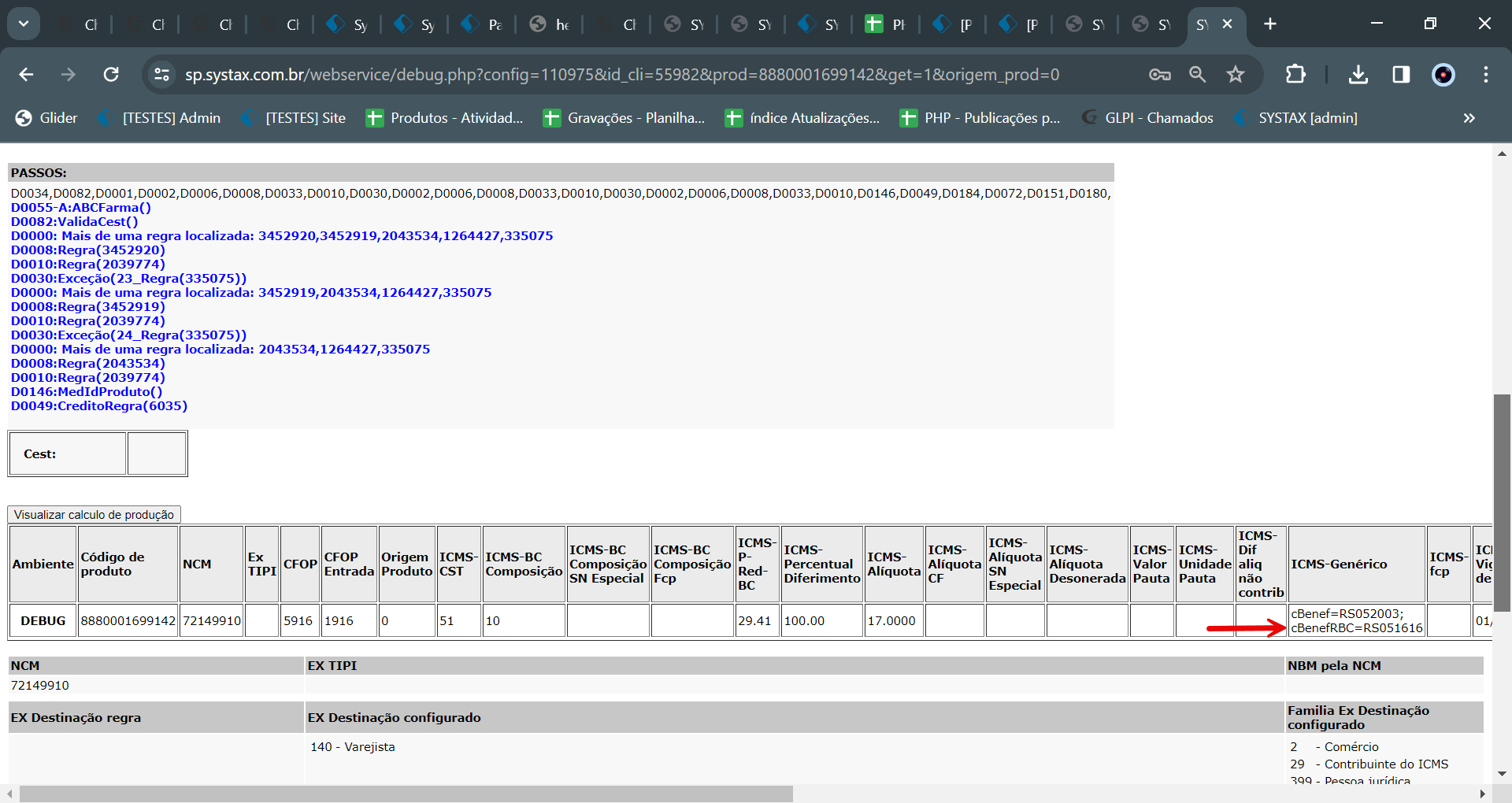

Quando falamos de UFs que possuem tabela Cbenef, ambas essas regras possuem o chamado código Cbenef, a critério da UF, e quando uma regra com esse código é aplicada no cálculo, no retorno no campo genérico do ICMS traz a variável código CBenef = UFXXXXX, sendo UF preenchido automaticamente pelo sistema conforme a UF da regra.

Com isso, quando aplicava o critério de desempate e aplicava a regra de CST 51, no campo genérico trazia o código CBenef relativo à regra de CST 51, ignorando a marcação da regra do CST 20.

Atualmente esse retorno mudou, conforme a publicação da Nota Técnica 2019.001, versão 1.61.

Com a implementação da melhoria, foi adicionada uma nova variável, chamada “cBenefRBC”, com a função de, mesmo após descartar a regra de CST 20 por conta do critério de desempate, ainda trazer no campo genérico o código CBenef referente à essa regra.

Segue exemplo do novo retorno:

[URL]

Com isso, trazemos informações mais detalhadas para o cliente, respeitando a documentação da Nota Técnica.

Returno of cBenefRBC

By Carlos Dupim Jr.

For a product and scenario that can be subjected to a tax rule with CST 51 (ICMS deferment) and CST 20 (reduction of calculation base), the system will apply, by the tiebreaking criteria of most beneficial tax rule, the one with CST 51.

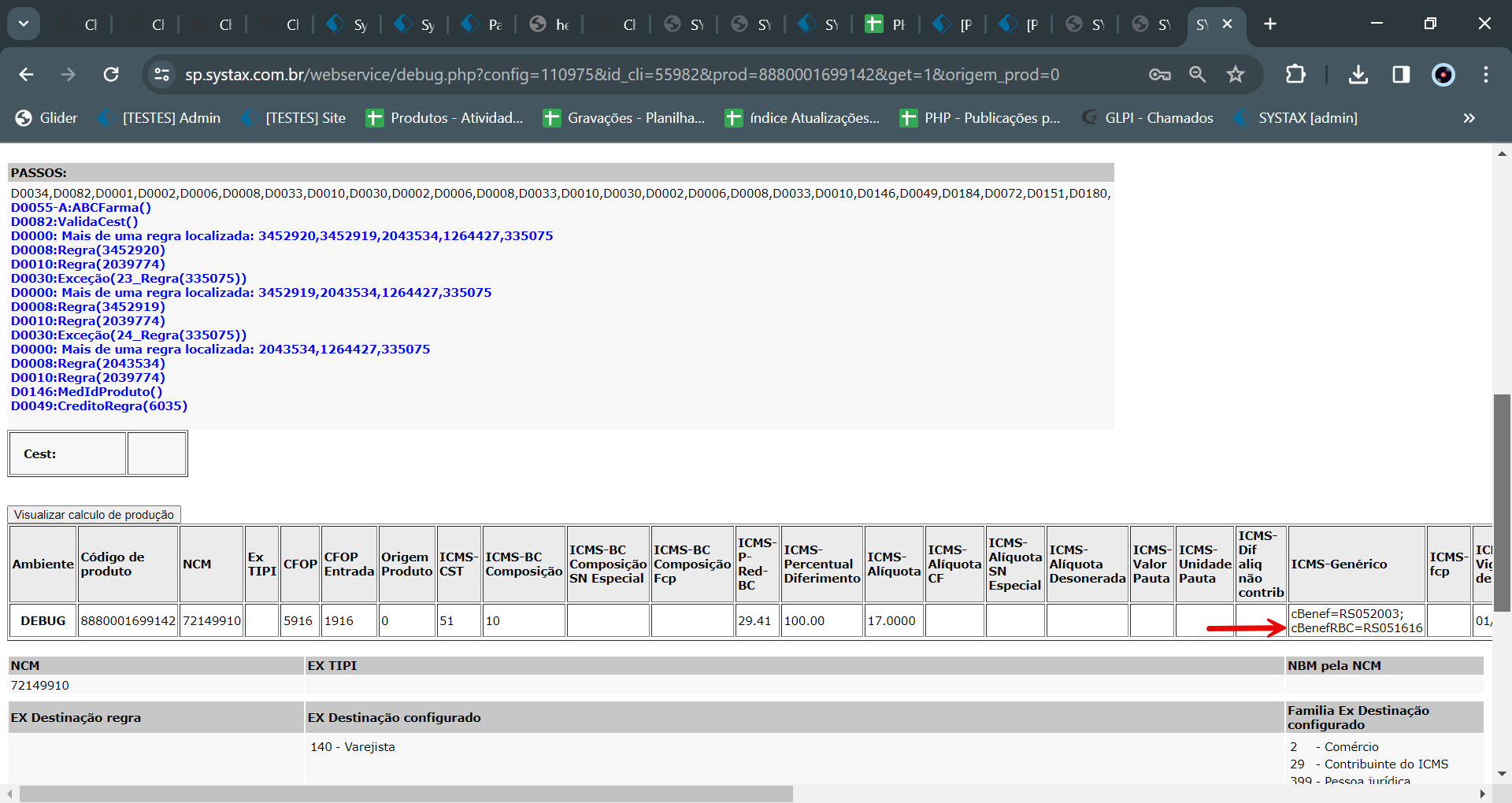

When we’re dealing with States that have a cBenef spread sheet, both rules have what is called a cBenef code, according to each State’s own spread sheet, and when a tax rule with said code is being applied to the calculation, in the ICMS “generic” field there will be a variable called cBenef = UF XXXXX, with UF being the State’s postal abbreviation, automatically determined according to the tax rule configuration.

That way, when the tiebreaking criteria was applied and the tax rule with CST 51 was chosen, in that “generic” field was the cBenef code present in the tax rule with CST 51, ignoring the code from de CST 20 tax rule.

Currently, this has changed, according to the publication of the Technical Note 2019.001, version 1.61, that now requires that, even though it’s not being used for the calculation, the code of the applicable tax rule with CST 20 must be present.

With the implementation of this new improvement, we added a new variable, called “cBenefRBC”, for the purpose of, even after the CST 20 tax rule being discarded over the more beneficial one, bringing its cBenef code alongside the other one, in a separate variable.

Here’s an example of the new information being returned:

[URL]

This way, we bring more detailed information to our clients, respecting the determinations of the Technical Note published.

| Versão do documento: 56 | Publicação: 3/8/2024 8 |